In a country where informal commerce dominates economic activity, Zimbabwe’s digital payments ecosystem has historically served established businesses better than individuals and small informal traders.

Most platforms and bank payment gateways have enabled online transactions for registered companies, but ordinary Zimbabweans selling products through WhatsApp, Facebook, and Instagram have largely remained outside the formal online payments infrastructure.

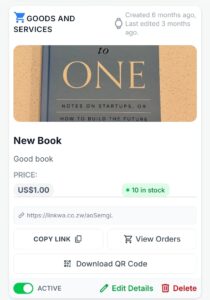

Linkwa.co.zw, launched by local technology company Pandawoga Innovate PBC, now allows individuals and small informal traders to generate payment links and QR codes that can be shared across platforms like WhatsApp, Facebook, and Instagram, turning social conversations into instant payment channels.

The platform allows users to register using only a Zimbabwean mobile number and create customized payment links for different purposes, from selling products and collecting donations to managing event registrations and group contributions.

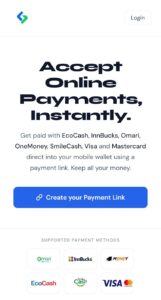

Each payment link generates a dedicated checkout page and QR code, which can be distributed digitally or even printed on flyers and invitations. Customers can then pay using EcoCash, InnBucks, OneMoney, Omari, SmileCash, as well as Visa and Mastercard.

For co-founder Tafadzwa Mapanzure, the launch reflects an effort to formalize digital commerce already happening informally across social platforms.

“Online commerce in Zimbabwe is not a future ambition. It is already happening every day across millions of WhatsApp threads and social media posts. What has been missing is the infrastructure layer that turns those interactions into proper transactions.”

That infrastructure includes tailored payment features depending on the user’s needs. Product sellers can track stock levels automatically, donation organizers can monitor contributors, and event managers can use an AI-powered multilingual registration tool that generates forms in English, Shona, or Ndebele before collecting payment.

The company says users retain 100 percent of their listed price, with buyers covering a 1 percent platform fee. Event transactions attract an additional fixed charge of USD 0.50.

First Impressions and User Interface

An independent test done by TechnoMag, as well as user experience reviews, shows that Linkwa’s biggest strength is its simplicity. The platform is clearly designed for mobile-first users who may not have advanced technical skills. The interface focuses heavily on accessibility rather than complexity, which is appropriate considering its target audience includes informal traders, churches, freelancers, event organizers, and small-scale entrepreneurs.

The workflow is straightforward:

- Sign up with a Zimbabwean mobile number.

- Create a payment link.

- Share the link or QR code.

- Receive payments.

There are no complicated merchant onboarding procedures or excessive verification barriers commonly associated with payment gateways.

The checkout pages appear clean and purpose-driven, avoiding clutter that often confuses first-time digital users. The integration of QR codes is particularly useful in Zimbabwe, where mobile wallet adoption is already widespread.

However, the platform’s minimalist design may also feel limited for advanced users seeking deep analytics dashboards, branding customisation, or complex e-commerce integrations.

Onboarding Experience

One of Linkwa’s strongest selling points is onboarding speed.

Unlike traditional payment gateways that may require:

- company registration documents,

- bank integrations,

- KYC reviews,

- merchant approval processes,

Linkwa appears to reduce onboarding to minutes using a phone number-based registration system.

This matters in Zimbabwe, where a significant portion of economic activity happens informally. Many traders operate entirely through WhatsApp groups and Facebook Marketplace listings without formal business structures.

For first-time users, the low barrier to entry could become a major adoption driver.

The onboarding philosophy resembles platforms such as:

But Linkwa localises the concept specifically for Zimbabwe’s mobile money ecosystem.

Features and Practical Use Cases

The platform’s feature set is surprisingly targeted for a relatively new entrant.

Key Features

- Payment links

- QR code generation

- Mobile wallet integrations

- Visa and Mastercard support

- Event registration tools

- Donations management

- Inventory tracking

- AI-powered multilingual forms

The most notable aspect is that Linkwa does not try to become a full e-commerce platform. Instead, it focuses on solving a narrower but critical problem: helping ordinary people accept payments digitally.

Innovation and Market Position

Linkwa’s innovation is not necessarily a technological invention. Payment links already exist globally. The innovation lies in localization.

The platform combines:

- Zimbabwean mobile wallets,

- informal commerce realities,

- diaspora payment needs,

- multilingual support,

- lightweight onboarding.

The above combination addresses a market segment that many traditional fintech products overlook.

The inclusion of AI-generated registration forms in English, Shona, and Ndebele is also notable. While not revolutionary, it reflects an understanding of local accessibility challenges.

Performance and Reliability

At this stage, Linkwa is still relatively new, which means long-term reliability and scalability remain unproven. According to the founders, the platform spent twelve months on integration and security preparation before public launch. That suggests operational caution rather than rushing to market.

So far, the app supports payments for:

- EcoCash,

- InnBucks,

- OneMoney,

- Omari,

- SmileCash,

- Visa,

- Mastercard

With this one can safely argue that the platform gives broad interoperability.

However, fintech platforms in Zimbabwe often face the following:

- mobile wallet downtimes

- currency volatility,

- network instability,

- regulatory shifts.

Linkwa’s long-term success will depend heavily on how consistently transactions are processed during peak demand periods.

Pricing Structure

Linkwa’s pricing model is aggressive and potentially disruptive.

Pricing Overview

- Basic Tier: Free

- Growth Tier: USD 1/month

- Standard Transactions: 1% fee paid by buyer

- Event Registrations: 1% + USD 0.50

For informal sellers, this is considerably more accessible than traditional merchant services.

The “seller keeps 100% of the listed price” positioning is psychologically powerful from a marketing standpoint, even though buyers ultimately absorb transaction costs.

Compared with regional competitors, Linkwa’s pricing appears competitive, especially for small-scale users.

Accessibility

Accessibility is one of Linkwa’s strongest areas.

The platform appears intentionally designed for:

- non-technical users,

- mobile-first environments,

- multilingual communities,

- informal sector operators.

The multilingual AI form generation is particularly relevant in Zimbabwe’s linguistic environment.

The absence of mandatory company registration could also widen digital inclusion significantly.

Privacy and Security Concerns

As with any payment platform, trust will be critical.

Linkwa states that payment processing is handled through licensed payment partners, which is reassuring. However, users will still want clearer long-term transparency around:

- data handling,

- fraud protection,

- chargeback management,

- dispute resolution,

- account recovery,

- transaction monitoring.

Since Linkwa handles financial transactions, its reputation will depend heavily on how effectively it manages scams, phishing risks, and user disputes.

New fintech platforms typically face an early-stage credibility challenge, especially in markets where users have experienced failed digital financial products before.

Strengths

What Linkwa Does Well

- Extremely easy onboarding

- Strong local market relevance

- Excellent support for mobile wallets

- Useful diaspora payment functionality

- Low pricing barrier

- Strong informal economy positioning

- Practical rather than over-engineered feature set

Weaknesses

- Limited long-term performance track record

- Unknown scalability under heavy usage

- Minimal advanced business tools

- Brand trust is still developing

- Heavy dependence on third-party payment infrastructure

- Potential regulatory exposure in Zimbabwe’s fintech sector

Linkwa is best suited for:

- informal traders,

- churches,

- event organisers,

- freelancers,

- tutors,

- content creators,

- small community groups,

- diaspora-funded projects.

Final Verdict

Linkwa.co.zw’s success will depend less on flashy innovation and more on execution, reliability, trust, and adoption within Zimbabwe’s informal economy. For a market where informal trade dominates and WhatsApp commerce is already mainstream, Linkwa arrives at an important moment.

Comments