In May 2018, headlines across Zimbabwe heralded a “mega-deal” that promised to revolutionise the nation’s energy sector. A USD$5.2 billion partnership with a South African firm, Nkosikhona Holdings, was set to transform the coal-rich Lusulu area of Hwange into a fuel-producing powerhouse, churning out 8 million liters of liquid fuel daily.

Today, that vision lies in ruins not because of market fluctuations or geopolitical shifts, but because the primary partner has effectively ceased to exist. Nkosikhona Holdings was struck off South Africa’s companies register for the most mundane of corporate failures, failing to submit annual returns.

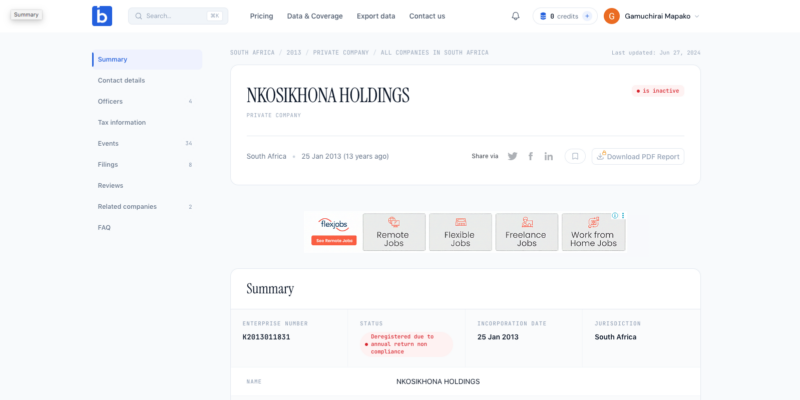

Recent records from South Africa’s Companies and Intellectual Property Commission (CIPC) reveal that Nkosikhona Holdings has been deregistered due to a consistent failure to comply with annual return requirements. In the world of corporate governance, deregistration is the ultimate administrative death sentence, signalling that a company is no longer a legal entity capable of holding contracts or conducting business.

The project did not begin operations, it was set for September 2018, with construction taking 3-4 years and is considered a failed or stalled venture by critics. Reports highlighted concerns over the company’s credibility, and as of late 2025, no progress was visible on the ground.

For Zimbabwe, the quiet dissolution of Nkosikhona is more than a regulatory footnote, it is a sobering food for thought moment regarding the vetting processes behind high-stakes national investments.

From the moment the Memorandum of Understanding (MoU) was signed between Nkosikhona and Verify Engineering, an agency under Zimbabwe’s Ministry of Higher and Tertiary Education, analysts expressed deep scepticism. The sheer scale of the $5.2 billion figure was at odds with the company’s digital footprint.

At the time of the signing, Nkosikhona Holdings was a private firm barely five years old. Investigations into its South African records showed a single director and a registered address in a light-industrial area, a far cry from the multi-billion-dollar infrastructure required for a sophisticated Coal-to-Liquid (CTL) plant. The company’s chief executive, Jacco Immink, had previously worked as a financial advisor. His co-director, Caroline Makhoro, listed previous experience as a cashier at a KFC franchise

The company was notably absent from the list of South Africa’s established liquid fuel producers, raising questions about whether it possessed the technical proprietary knowledge to execute such a complex extraction project.

A senior Zimbabwean minister at the time declined to disclose the shareholding structure of the joint venture, stating it was “not information of public interest”

Eight years later, with Nkosikhona Holdings deregistered and the Hwange plant unbuilt, that assertion appears, at best, overly optimistic.

The deal was often cited as a cornerstone of Zimbabwe’s “Open for Business” mantra. However, the secrecy surrounding the company’s background and the lack of a known history in the extractives sector created a vacuum of accountability.

Critics argue that the deregistration for non-compliance with annual returns which is a basic administrative task, is the most telling indicator of the company’s true standing. If a firm lacks the internal capacity to maintain its legal status in its home country, its ability to manage a $5 billion foreign infrastructure project becomes a mathematical impossibility.

The Nkosikhona case now joins a growing list of ambitious investments in Zimbabwe that have failed to materialise. It highlights a recurring theme in emerging markets: the “Memorandum of Understanding Trap,” where large-scale promises generate immediate political capital but lack the financial or technical bedrock to achieve final investment decisions.

It is important to remember and note that true economic resilience is built not through the signing of papers with unproven entities, but through rigorous due diligence and partnerships with established players capable of surviving more than a single regulatory cycle.

The company that promised to transform Zimbabwe’s energy future has, it seems, transformed nothing but its own status from active to archived.

Comments